")

Travel savings don’t happen by accident—they happen when you make them a priority.

Our family saved nearly $60,000 on a single income to spend five months in Europe, and we did it without debt or trust funds. Just a clear system, some discipline, and choices that lined up with our values.

In this post, I’ll show you the exact steps we’ve used for over 20 years of travel—before kids and with four in tow—so you can start saving smarter, avoid the stress of borrowing, and feel confident your next trip is fully paid for.

How To Grow Your Travel Savings

Growing your travel savings comes down to three things: knowing exactly what you can afford, getting specific with your goals, and setting up a system that makes saving effortless. These steps give you clarity, motivation, and a plan that actually works.

Work Out How Much Money You Can Save For Travel

You can’t plan the trip of your dreams without knowing your numbers. Start by writing down every expense, then decide what matters most, and build a household budget that reflects those priorities. Once you’ve got clarity, you’ll know exactly how much you can set aside for travel.

Write Down Your Expenses

The fastest way to get clear on your money is to write down every expense.

And yes, my friend, I mean every single one.

Those small purchases—like coffees, snacks, or the quick “just one thing” at the supermarket—often add up to a lot more than you think. That’s money that could be moving you closer to your travel fund.

You want to know your expenses inside out. Not roughly. Not “close enough.” Exactly. Because the clearer the picture, the easier it is to see where you can trim and where you’re doing fine.

Here’s a starting list of what most households juggle each month:

- Mortgage or rent

- Utilities (electricity, water, gas)

- Internet and phone

- Groceries

- Debt repayments

- Insurance (car, home, health, life)

- School fees and after-school activities

- Fitness or gym memberships

- Haircuts and personal care

- Restaurants, cafes, and takeaways

Once you’ve listed everything, add it all up. What’s your total spend each month? Now compare it with your household income. The number left over—if there is one—is your saving potential.

If that leftover figure looks small, don’t panic. Even a little adds up when you save it consistently. And if it looks bigger than you expected, congratulations—you’ve just found the breathing room that could fast-track your next trip!

Writing down your expenses isn’t about guilt. It’s about awareness. When you know exactly what’s leaving your account, you’re in control. And control is what makes growing a travel fund feel achievable instead of overwhelming.

I know this is a big job… it may even feel like a drag or too overwhelming to even start. But don’t skip this part. Give yourself the best chance possible and take the time to do it. It’s possibly the most eye-opening step. You’ve got this.

Establish Your Priorities

Travel doesn’t happen by accident—it happens because you make space for it.

That means asking the hard questions: is travel a top priority for your family, or just something you’d like to squeeze in once a year? Being honest here makes all the difference.

If travel is high on your list, you’ll need to frame every money choice around it. What’s worth giving up, and what’s not?

For us, we cut back on a lot of things to make travel happen. Restaurants are nice, but they don’t mean as much to us as exploring a new country together. But that may not be the case for every family. Your list might look different, and that’s OK.

Think about your household income, your other goals, and where travel sits among them. Are you paying down debt? Saving for a home? Juggling school fees? Decide how much you’re willing to put aside for travel each month, and work to find a number that feels realistic and aligned with your own goals and values.

This is where big changes can happen if you want them to. Maybe you swap the gym membership for YouTube workouts. Or you cut back on subscription services. Some families even downsize their home to free up income for more experiences.

It’s about weighing needs versus wants and being brave enough to let go of things that don’t matter as much. I know, big call, and it’s not for everyone.

Make sure you don’t cut out everything fun, either. If your morning coffee genuinely sparks joy, keep it. But if it’s just habit, a thermos from home might do the job.

Reassess, re-calculate, and you’ll see how much extra can go towards your travel savings.

Priorities shape your future. If travel is what you value, give it the space it deserves. This is the part where real shifts happen—and where travel goes from being a wish to becoming your reality.

Build Yourself A Household Budget

Don’t panic at the word “budget.”

It’s not about rules and restrictions—it’s simply a tool to help your money go where you want it to go. And when that goal is travel, a budget actually becomes something exciting (yes, it really does!).

Start by mapping out your fixed expenses. These are the non-negotiables you must cover each month. Some examples are:

- Rent or mortgage

- Utilities (electricity, water, gas, internet, phone)

- Insurance

- Debt repayments

- School fees or childcare

- Groceries and fuel

Add these up and set that money aside first. That way, the essentials are always covered.

Now, make room for emergency savings. Even a small buffer can save you from dipping into credit cards if something unexpected happens. And if you’re carrying consumer debt, focus on knocking that down too. Travel feels so much better when you’re not coming home to financial stress.

Next, decide how much you’re comfortable with for discretionary spending. These are the flexible costs—eating out, gym memberships, family activities. Track these carefully and stick to your chosen limit. This is where overspending usually sneaks in, so a bit of discipline goes a long way.

Finally, see what’s left. This is the fun part—because this is what you get to allocate to your travel savings. The more detail you put into your budget now, the faster those savings grow.

💡 If you’d like step-by-step guidance on setting up a budget that actually works, my Freedom Budgeting Course walks you through the exact system I use. It’s designed to take the stress out of budgeting and help you focus on your real goals—like travel.

Map Out Your Overall Travel Vision

Dreaming is fun, but planning is what makes travel actually happen.

By mapping out your vision in detail, you’ll know exactly what you’re saving for—and why. The clearer the plan, the easier it is to stay motivated and make smart money choices along the way.

Get Specific With Your Travel Goals

Vague goals don’t get funded. Specific ones do.

Ask yourself:

- Where do you want to go? Paris in spring? Japan during cherry blossom season? A week in Bali?

- How long for? A weekend escape, two weeks abroad, or a full month away?

- What kind of trip do you want? Relaxing, adventurous, cultural, luxurious, or budget-friendly?

- When will you go? Give yourself a timeframe. “Next July” is far more motivating than “someday.”

Now start a rough itinerary. You don’t need exact bookings, just a sketch of the big things:

- Flights (for all family members)

- Accommodation (type and price range)

- Food (mix of cooking and eating out)

- Activities or attractions

- Transport (car hire, public transport, or transfers)

Why it matters:

- A plan makes the trip feel real.

- It helps you estimate costs early.

- It keeps motivation high because you can picture yourself there.

💡 Our family has learned that “when” you go can matter just as much as “where.” We love shoulder or down seasons. The Faroe Islands in autumn, for example, were magical—still stunning without the summer crowds, and much lighter on the budget.

Dig A Little Deeper Into Your Target Destination

Once you’ve got the broad vision, it’s time to dig into the details. Research now prevents financial shocks later.

Key things to look at:

- Accommodation

- Average nightly rates for your travel dates.

- Differences between peak and off-peak seasons.

- Options that suit your family—hotel, Airbnb, or holiday park.

- Average nightly rates for your travel dates.

- Food

- Will you have a kitchen and cook some meals?

- Or will you mostly eat out?

- What’s the average price of restaurants or cafes in your destination?

- Will you have a kitchen and cook some meals?

- Flights

- Typical costs at the time of year you want to travel.

- How much flexibility in dates could save you money.

- Budget vs full-service airlines.

- Typical costs at the time of year you want to travel.

- Activities

- Must-do items on your list (theme parks, museums, tours).

- Free or low-cost options (parks, hikes, street markets).

- Cost of entry tickets for adults and kids.

- Must-do items on your list (theme parks, museums, tours).

- Transport

- Hiring a car (fuel, insurance, parking).

- Public transport passes (buses, trains, metro).

- Private transfers (airport pick-ups, day tours).

- Hiring a car (fuel, insurance, parking).

💡 In Finland, almost every activity was pricey. We chose to put our money into unforgettable experiences like dog sledding and searching for Santa. To balance it, we cooked most meals ourselves and treated the kids to smaller things—hot chocolates at cafés or a shared plate of reindeer fries. It’s all about picking what matters most to your family.

Determine How Much You Need To Save In Total

Now comes the big question: how much money will this trip take? Without a number, saving feels vague. With a number, you’ve got a clear target to aim for.

Here’s how to calculate it:

- Add up your big categories:

- Flights

- Accommodation

- Food and drinks

- Activities and attractions

- Transport

- Travel insurance

- Flights

- Add a buffer:

- Solo travellers: around $500

- Families: at least $1,000

- This covers surprises, emergencies, or last-minute splurges.

- Solo travellers: around $500

- Set a daily budget:

- Meals

- Local transport

- Fun money for snacks, souvenirs, or unexpected opportunities

- Multiply by the number of travel days to get a realistic figure.

- Meals

- Decide your high-low balance:

- What’s worth splurging on? (e.g. a bucket-list tour, special dinner).

- Where can you save? (e.g. simple meals, budget stays, free experiences).

- If you’re new to this, check out my post on High-Low Travel—it’s all about putting money where it counts.

- What’s worth splurging on? (e.g. a bucket-list tour, special dinner).

- Lock in your total goal:

- Add your categories, your buffer, and your daily budget.

- This final number is your travel savings target.

- Add your categories, your buffer, and your daily budget.

💡 During our five months in Europe, our emergency fund was used again and again. We dipped into it for things that were over budget, for doctor visits that weren’t worth claiming on insurance, and other unexpected costs. Honestly, I don’t think we’ve ever been on a trip where we didn’t need that buffer. Something always comes up, and it’s what kept our travels stress-free.

Mapping out your travel vision isn’t just daydreaming—it’s the foundation of your trip.

- You’ve defined where, when, and what kind of trip you want.

- You’ve researched the real costs of your destination.

- You’ve calculated a savings target with room for flexibility.

- You’ve seen how real families (like ours) make trade-offs to make it work.

Now you know exactly what you’re aiming for. And that clarity is what transforms travel from a wish into a plan. Every dollar you save from here on out has a job—and that job is getting your family onto that plane.

Set Up A Killer Saving System

This is where your trip goes from dream to plan.

A savings system removes the guesswork, keeps you motivated, and makes saving consistent. With the right structure, you’ll be surprised how quickly your travel fund grows.

Establish A Dedicated Travel Savings Account

Step one: separate your travel money from everything else. If it sits in your everyday account, it’ll disappear on groceries, petrol, or takeaway dinners before you even notice.

- Open a dedicated account just for travel.

- Don’t mix it with your everyday accounts or emergency savings.

- Keep it clean, clear, and easy to track.

For extra motivation, give it a name that makes you smile every time you log in. Instead of “Savings Account 2,” call it:

- “Cocktails by the Pool”

- “Disney 2026”

- “Italy Pizza & Gelato Fund”

💡 When we were saving for our five-month Europe trip, we called the account “The Big Trip.” Every time I saw that name and watched the balance grow, it felt more real than just staring at a generic savings account. Those little details really do make a difference.

Calculate Your Finances Against Your Departure Date

Now it’s time to connect your savings target with your travel date. This step keeps your plan grounded and realistic.

Here’s the process:

- Find your estimated trip cost you worked out previously.

- Divide that number by the number of months until you want to leave.

- The result is your monthly savings target.

Examples:

- $5,000 trip ÷ 5 months = $1,000 per month

- $5,000 trip ÷ 12 months = $416 per month

- $5,000 trip ÷ 18 months = $277 per month

This monthly breakdown becomes your personal trip savings plan. If your number feels too high, you’ve got two options:

- Push your departure date further back, giving yourself more time to save.

- Adjust your trip plan to reduce costs.

💡 For our Europe trip, we started years before we even knew the exact date. We started by putting aside just $50 per pay into our “Big Trip” account. As the months went on, we slowly increased the amount. Around 2 years out, we ran the above calculations properly to see what we needed to save each month to hit our target. We reassessed again at 12 months, then at six months, and then monthly as the trip approached. No guesswork, no stress—just a clear plan that worked for both long-term and short-term goals.

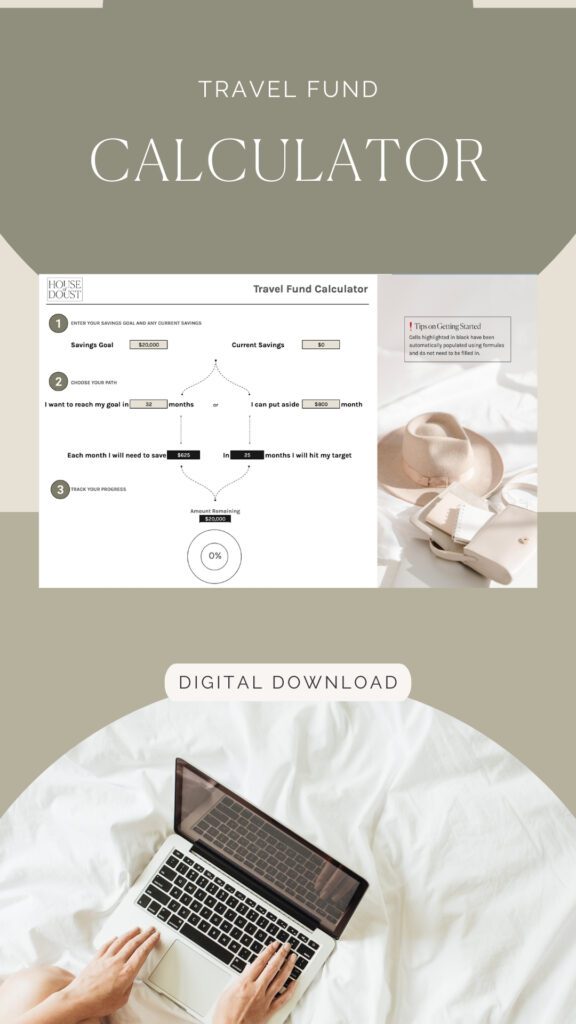

💡 Pro Tip Want to skip the guesswork? Grab my free Travel Fund Calculator. Pop in your trip cost, timeline, and budget, and it’ll crunch the numbers for you—showing exactly how much to set aside each month to hit your goal.

Automate Automate Automate!

Here’s the magic secret: automation.

Set up a direct deposit from your bank to your travel account for the day after payday. That way:

- The money moves before you can spend it.

- You don’t need to rely on willpower.

- You avoid reaching the end of the month with nothing left to save.

Think of it as paying your future self first. Your travel dreams get priority, and the rest of your pay takes care of bills and daily life (bills and daily life should be taken care of already, inside that household budget you created earlier… yes, the step you probably wanted to skip).

💡 We’ve used this trick for every major trip. Without automation, saving slips through the cracks. With it, the money just grows—no effort required.

Challenge Yourself To Boost Your Travel Fund Now And Then

Automation covers the basics, but small boosts give you momentum. They’re like secret shortcuts to reaching your goal sooner.

Ideas to try:

- Skip a meal out: If everyone’s tired and grumpy, stay in and pop that $60 into your travel fund instead. That’s one more restaurant meal you can enjoy on holiday.

- Redirect bonuses or refunds: Tax refunds, work bonuses, or unexpected cash—send it straight to your travel fund before it blends into everyday spending.

- Swap activities: A home movie night instead of the cinema could save $100+ for a family.

- Sell unused items: Kids’ clothes, old toys, or furniture you don’t need—convert clutter into travel cash.

💡 In the lead-up to trips, we often go extra frugal. When the kids ask for ice cream (every single time we drive past a picture of one), we ask, “Would you like an ice cream now, or an extra ice cream in Thailand?” The holiday usually wins.

Keep Yourself Motivated Along the Way

Saving for months—or years—can feel like a real grind sometimes. You’ve gotta keep motivation alive with small tricks:

- Track progress visually: Use a thermometer chart, jar, or digital tracker.

- Celebrate milestones: Reward yourself (cheaply) when you hit 25%, 50%, and 75% of your goal.

- Keep your destination visible: Photos on the fridge, a screensaver of your dream spot.

- Make it a family project: Let the kids colour in progress charts or choose which activity you’ll splurge on.

Every little reminder helps keep the excitement alive.

Build in Flexibility

Life doesn’t always stick to plan. Cars break down, school fees pop up, bills jump. That’s why flexibility is always going to be needed.

- Protect your emergency fund first. Always.

- Don’t touch your travel account unless it’s absolutely necessary.

- Be willing to adjust your savings timeline if life throws curveballs.

A killer saving system isn’t about cutting out joy—it’s about putting the right tools in place so your money works for you.

- Separate your savings in a dedicated account.

- Name your account for motivation.

- Reverse engineer your timeline so your monthly goal is clear.

- Automate transfers so saving happens without thought.

- Challenge yourself to add extra when you can.

- Stay motivated with progress trackers and family involvement.

- Protect your buffer so surprises don’t derail you.

Do this, and you won’t just dream about travel—you’ll actually board the plane, knowing every dollar was part of a plan.

And while you’re saving, don’t forget to map out your travel budget too. Every hard-earned dollar deserves to be used wisely once you’re away. It’s easy to overspend on meals, activities, and souvenirs, and end up back in debt.

A travel budget keeps your savings working hard for you on the road. I’ve written a full guide on creating a travel budget to help with this next step.

Unique Ways To Grow Your Travel Savings

Feeling super motivated and want to get creative, boosting that travel fund?

These ideas might not work for every family, but the key is to pick what feels doable for you and make it part of your saving rhythm.

Start Collecting Points And Miles

Loyalty points are like secret money sitting in your wallet. The trick is to actually use them strategically.

- Be deliberate with your program. Know which airline or alliance will get you to your chosen destination, and focus your loyalty there for the time being. If you collect random points across multiple programs, you’ll end up with a lot of small balances that don’t get you very far.

- Link everyday spending. Groceries, fuel, even online shopping often have partner programs. Make sure you’re earning points on purchases you’d be making anyway.

- Consider a rewards credit card if you can pay it off in full every month. Used responsibly (I can’t emphasise this enough, if you can pay it off in full each month), this can speed up your points balance without costing you interest.

💡 The best use of points is nearly always flights. Securing reward seats can make a huge difference to your travel budget. Keep your points focused on getting you in the air, not a new toaster.

Sell Items Online

One family’s clutter is another person’s treasure. Selling unused items is one of the fastest ways to give your travel fund a boost.

- Bikes or toys they’ve outgrown.

- Baby gear gathering dust in the garage.

- Furniture, appliances, or hobby gear you’re not using.

Platforms like Facebook Marketplace, Gumtree, or eBay make it easy. Even small amounts add up—$20 here, $50 there. That’s a night’s accommodation or a day of meals sorted.

💡 When we were preparing for Europe, we sold our pram and some other bigger items. It felt so good seeing clutter turn into a stronger travel fund.

Save your tax returns

If you happen to get a tax return, instead of letting it get lost in the shuffle of bills and daily life, send it straight to your travel account.

- Treat it as “bonus money” you never had.

- Even a modest return of a few hundred dollars can cover flights for a child or a whole week of food in some destinations.

- Combine it with other windfalls (work bonuses, birthday cash, rebates) and you’ll see a healthy jump in your savings.

💡 For our Europe trip, we saved for nearly four years. Using tax returns from several years in a row gave our budget a real boost. That money went straight into the “Big Trip” account, and it helped us stay consistent even when regular savings felt slow.

Live off one wage

I know… this is a big, bold strategy, but it’s also the one that moves the needle fastest.

- Commit to living on just one income for a set time.

- Funnel the other income directly into your travel fund.

- Even trying this for a few months can create huge savings momentum.

Yes, it’s a challenge—especially with rising costs of living. But if travel is a top priority, this approach forces you to strip back expenses, reassess priorities, and accelerate your timeline.

💡 We lived on one wage for the entire time we were saving for Europe. It wasn’t always easy, but we managed to save tens of thousands of dollars for a five-month trip as a family of six. The sacrifices were absolutely worth it when we were finally boarding that plane.

Other Quick Wins

There are countless small tweaks that can give your travel fund a boost. Two of the most effective:

- Mini challenges like no-spend weekends, rounding up purchases, or matching small indulgences with equal savings.

- Cutting recurring costs like unused subscriptions, overpriced phone plans, or gym memberships you rarely use.

I’ve written more about these in a separate post—check out 30 Creative Ways to Save Money for Travel for a bigger list of ideas you can try.

Growing your travel fund doesn’t have to feel slow or boring. With some creativity and discipline, you can speed things up and actually enjoy the process along the way.

- Be strategic with points and miles.

- Sell clutter for quick wins.

- Treat tax returns and bonuses as holiday money, not bill money.

- Go bold with one-income living if you can.

- Layer in creative challenges and cut recurring costs.

💡 Our family’s Europe trip happened because we pulled these levers all at once. We used our tax returns year after year, sold off the bigger baby gear, and kept ourselves to one wage. It wasn’t always glamorous, but watching that account grow felt incredible—and spending that money on memories was the best reward.

Each of these strategies adds fuel to your savings plan. Alone they’re helpful; together they can change the game. Your travel account grows faster, your trip feels closer, and your family gets used to prioritising what really matters.

FAQs

How Much Should You Save For Travel?

How much you should save for travel depends on your trip’s length, style, and destination. Start by adding up the big costs—flights, accommodation, food, activities, transport, and insurance—then add a buffer of $500–$1,000 for families. Having a clear total gives you a target and helps avoid debt after your trip.

How Do I Make Travel Savings?

Making travel savings starts with clarity and consistency. Open a dedicated account, automate transfers after payday, and track your expenses. Prioritise travel in your budget by cutting back on non-essentials that don’t matter as much. Even small, steady contributions add up over time, turning your travel dreams into realistic, bookable plans.

Where Should I Put Money To Save For A Vacation?

The best place to put money for a vacation is a separate savings account. Keeping it away from your everyday funds reduces the temptation to dip into it. Choose an account with no card access if possible, and give it a motivating name so you’re reminded of your goal each time you see it.

Can I Open A Travel Savings Account?

Yes, you can open a travel savings account, and it’s one of the best strategies. Having a dedicated account keeps your travel money separate from everyday spending. Many banks make it easy to set up online, and naming the account after your destination can keep you motivated as you watch the balance grow.

Should You Have A Travel Fund?

Yes, having a travel fund is essential if you want to travel without debt. A dedicated fund allows you to plan ahead, save gradually, and enjoy your trip without financial stress. It also gives you freedom to say yes to experiences, knowing you’ve already set money aside just for that purpose.

Is It Ok To Spend All My Money On Travelling?

Spending all your money on travelling isn’t wise. Travel should add to your life, not create financial stress when you get home. Save intentionally, build an emergency buffer, and make sure essentials like bills and debt repayments are covered first. Then enjoy using your travel fund guilt-free, knowing it’s money you’ve planned for.

What Is The Best Way To Travel With Money?

The best way to travel with money is to mix payment options. Bring a travel debit or credit card with no international fees, carry a small amount of local cash, and keep a backup card in case of emergencies. Avoid relying on just one option—it’s safer and more convenient to have multiple ways to pay.

How Much Does The Average Vacation Cost?

The average vacation cost varies widely, depending on destination, duration, and travel style. A local week away might be under $2,000, while international family trips often reach $5,000–$10,000 or more. The key is to calculate your own expected costs—flights, accommodation, food, transport, and activities—so you know exactly what you’ll need for your trip.

How Much Money Should I Save For A Month-Long Trip?

How much to save for a month-long trip depends on where you’re going and how you travel. A budget trip might be $3,000–$5,000, while a more comfortable or international trip could reach over $10,000. Work out your daily budget for meals, transport, and activities, then multiply by the number of days.

How Much Money Should I Have Saved To Travel For 6 Months?

Travelling for six months requires a solid savings plan. Depending on your destination and lifestyle, you may need anywhere from $15,000 to over $30,000, especially with kids. Long-term travel works best when you budget for accommodation, food, insurance, and daily expenses, plus a generous buffer. The clearer your plan, the more realistic your savings target will be.

Is It Possible To Save $10,000 In 6 Months?

Yes, it’s possible to save $10,000 in six months, but it requires discipline. You’d need to set aside about $1,600–$1,700 per month. That may mean cutting back on non-essentials, finding extra income, or both. If that number feels unrealistic, extend your timeline—saving steadily is better than stretching your budget too thin.

Wrapping It Up: How To Grow Your Travel Savings

Growing your travel savings isn’t about luck—it’s about clarity, priorities, and a system that works. When you know your numbers, set clear goals, and build a savings routine, you can travel without debt and enjoy the trip even more.

The key is making choices that line up with what matters most to you. Our family saved nearly $60,000 on a single income for five months in Europe—it wasn’t easy, but every dollar had a job, and every choice moved us closer to the trip.

Once you’ve mapped your budget and vision, saving up for a trip doesn’t feel impossible—it becomes a clear, step-by-step plan. If you’re ready to keep working towards your next trip, check out my guide on easy tips to afford your next family vacation—it’s packed with simple, practical ideas to cut everyday costs and free up more money for travel.

Rachel Doust is the founder of House of Doust, where she shares practical tips on family travel and smart budgeting for parents who want meaningful adventures without financial stress. A mum of four and a lifelong traveller, Rachel has a heart for helping parents feel more confident about travel and money through honest advice, real-life experience, and easy-to-use resources. When she’s not on the road, she’s busy creating tools that make trip planning simpler for busy families.

love this post? share it!

")